The self-funded benefits market is entering a new era, showing significant signs of strain after several years of poor performance. Multiple large reinsurers exited the medical stop-loss market in 2026, and Symetra reported that the market’s 2025 loss ratio hit a record high 91%.

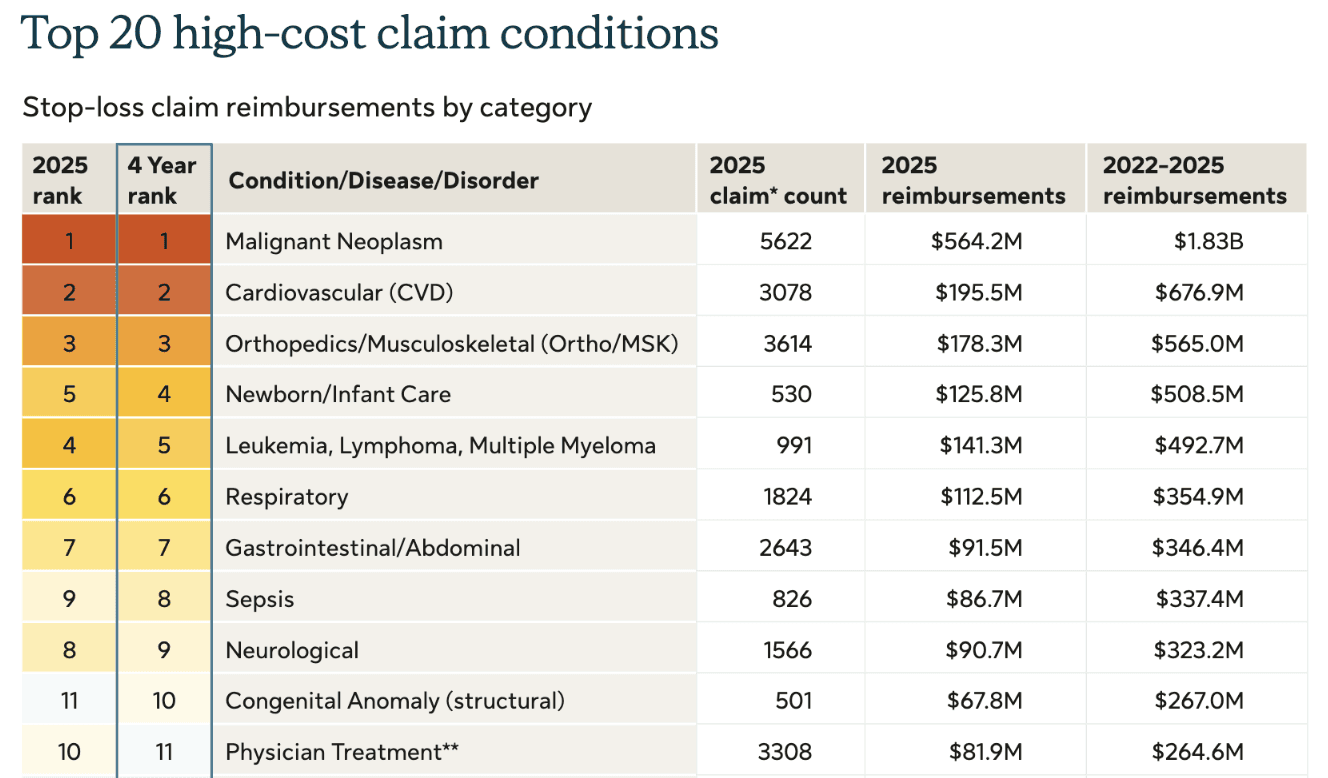

The pressure is coming from multiple directions. First, innovative therapies are expanding what medicine can do, but these treatments are straining budgets. Employers and carriers alike are feeling the impact of everything from greater GLP-1 utilization to increasingly expensive cell and gene therapies coming to market. For example, Sun Life’s 2026 high-cost claims analysis found that million-dollar-plus claims are up 46% since 2022. Second, billing dynamics are changing because of both AI and increasing provider consolidation. In its 2026 Medical Cost Index report, Milliman flagged AI-enabled revenue-cycle tools and higher diagnostic intensity within hospital-owned providers as notable contributors to the expected 2026 trend rate of 7.9%, as providers adopt technology to improve charge capture, coding, documentation, and denials management. When combined with the downward pressure on stop-loss premiums created by new entrants pricing aggressively for growth, it is no surprise that the industry is facing financial headwinds.

However, challenging markets reward better operators. Organizations that are creative, resilient, and adaptive can come out of today’s challenging climate stronger than they entered it.

For employers, the mandate is visibility. Trend rates can no longer be managed through renewal negotiations alone. Employers need earlier access to claims data, a clearer view into the root causes of spend, and the ability to connect plan design, vendor performance, care navigation, and stop-loss strategy into one operating model.

For carriers and risk partners, the opportunity is to move beyond opaque, commodity stop-loss products. The market is already shifting toward stronger underwriting discipline, unbundled models, clearer contracts, alternative risk structures, and more active cost management. Continued investments in providing higher-value care, earlier interventions and support, and reducing waste offer risk partners the ability to differentiate themselves through value-additive services.

For plan members themselves, the best answer is not blunt cost shifting. Higher deductibles and premiums may reduce employer exposure on paper, but they rarely solve the underlying problem. The most sophisticated employers are helping members reach higher-value care earlier through member outreach, navigation, second opinions, in-network access support, and interventions before complex conditions become catastrophic.

For organizations willing to rethink their approach to self-funding, this reset creates an opening to build more transparent, proactive, and resilient financing models. Amera supports that shift by providing the claims infrastructure that makes risk visible earlier, enables targeted intervention, and gives employers and partners the data foundation they need to manage self-funded healthcare with greater precision.

Download the high-resolution PDF of our TPA Ecosystem Map